How Much Student Debt Is There? At HOW.EDU.VN, we recognize the burden of student loan debt and offer expert guidance to navigate these complex financial challenges, providing strategic advice and support for debt management and financial planning. By exploring strategies for repayment, consolidation, and potential forgiveness programs, we empower individuals to regain control of their finances, reduce financial stress, and plan for a secure future. Student loan burden and college affordability are key concerns we address.

1. Understanding the Landscape of Student Loan Debt

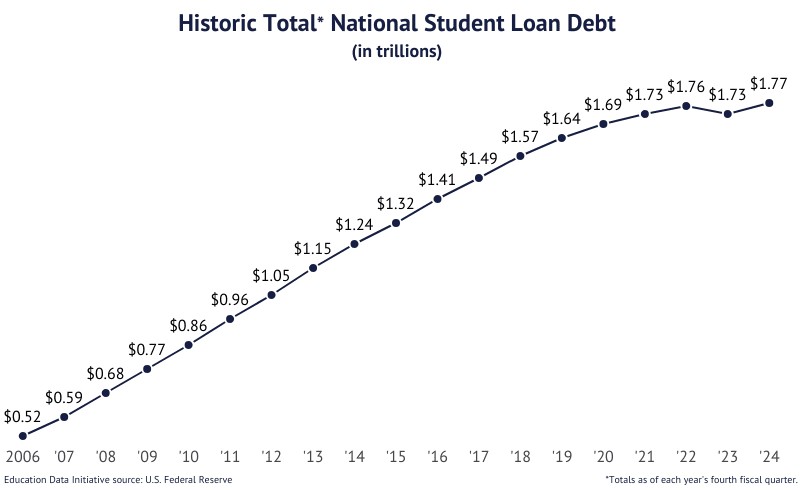

Student loan debt has become a significant issue in the United States, impacting millions of individuals and the economy. In this section, we delve into the current statistics and trends surrounding student loan debt, offering a comprehensive understanding of the problem.

1.1. Current Student Loan Debt Statistics

As of 2024, the total student loan debt in the United States stands at approximately $1.777 trillion. This staggering figure reflects the cumulative debt of millions of Americans who have pursued higher education through loans.

- Total Student Loan Debt: $1.777 trillion

- Federal Student Loan Debt: $1.693 trillion

- Private Student Loan Debt: $138.502 billion

1.2. Composition of Student Loan Debt

The vast majority of student loan debt is held by the federal government. Federal student loans account for approximately 92.2% of all student loan debt, while private student loans make up the remaining 7.79%.

- Federal Share: 92.2% ($1.693 trillion)

- Private Share: 7.79% ($138.502 billion)

1.3. Average Student Loan Debt Balance

The average federal student loan debt balance is $38,375. When including private loan debt, the total average balance can reach as high as $41,618. These figures highlight the substantial financial burden faced by individual borrowers.

- Average Federal Debt: $38,375

- Total Average Debt (Including Private): Up to $41,618

1.4. Default Rates

As of the fourth financial quarter of 2024, 4.86% of federal student loan dollars were in default. The default rate for private student loans was 1.61% as of the first quarter of 2024. These rates indicate the challenges many borrowers face in repaying their loans.

- Federal Loan Default Rate (2024 Q4): 4.86%

- Private Loan Default Rate (2024 Q1): 1.61%

1.5. Debt for Bachelor’s Degrees

The average public university student borrows $31,960 to attain a bachelor’s degree. This debt represents a significant investment in their future, but it also poses a considerable financial challenge upon graduation.

- Average Debt for Public University Bachelor’s: $31,960

2. Trends in Student Loan Debt

Analyzing trends in student loan debt provides insights into how the situation is evolving over time. This section examines recent changes in student loan debt balances, growth rates, and other key indicators.

2.1. Recent Increases in Student Loan Debt

In 2024, student loan debt experienced a resurgence in growth following a year-over-year decline in 2023. The fourth quarter of 2024 saw a 2.77% increase in national student loan debt compared to the previous year.

- Q4 2024 YoY Increase: 2.77%

2.2. Federal vs. Private Loan Growth

Federal student loan debt increased by 2.27% in the fourth quarter of 2024, while private student loan debt totaled $138.502 billion. The increase in federal debt accounted for 75.9% of the total increase in all student loans, highlighting the dominance of federal loans in the market.

- Federal Loan Increase (Q4 2024): 2.27%

- Private Loan Total (Q1 2024): $138.502 billion

2.3. Declines in Student Loan Debt in 2023

For the first time, total student loan debt declined from one year to the next between 2022 and 2023. In the fourth quarter of 2023, national student loan debt declined by 1.98% year-over-year.

- Q4 2023 YoY Decline: 1.98%

2.4. Federal and Private Loan Decreases in 2023

In 2023, federal and private student loan debt combined decreased by $34.9 billion. Federal student loan debt alone decreased by $32.3 billion, indicating a significant shift in the student loan landscape.

- Total Decrease in 2023: $34.9 billion

- Federal Decrease in 2023: $32.3 billion

2.5. Slower Growth in the 2020s

While total student loan debt grew in 2022, the annual growth rate was slower compared to the previous decade. Between the first quarter of 2020 and the first quarter of 2023, student loan debt accumulation decreased by an average quarterly rate of 31.4%.

- Average Quarterly Decrease: 31.4%

3. Impact of Student Loan Debt Relief Measures

Various student loan debt relief measures have been introduced to alleviate the financial burden on borrowers. This section explores the impact of these measures, including interest freezes, loan forgiveness programs, and the CARES Act.

3.1. Federal Student Loan Interest Freeze

Federal student loan interest was set to 0.0% for most federal loans until after August 31, 2023. This interest freeze provided significant relief to borrowers by preventing their loan balances from growing due to interest accrual.

- Interest Rate: 0.0% until August 31, 2023

3.2. Support for Loan Forgiveness

There is considerable public support for student loan forgiveness. According to surveys, 55% of Americans support cancellation of up to $10,000 per borrower in federal student loans, while 47% support cancellation of up to $50,000 per borrower.

- Support for $10,000 Cancellation: 55%

- Support for $50,000 Cancellation: 47%

3.3. Opposition to Loan Forgiveness

Despite the support for loan forgiveness, 31% of Americans oppose the idea. The debate over student loan forgiveness continues to be a contentious issue in the United States.

- Opposition to Loan Forgiveness: 31%

3.4. Impact of the CARES Act

Introduced between the second and third financial quarters of 2020, the CARES Act provided student loan debt relief that affected an estimated 35 million borrowers. The act led to a significant decrease in the amount of student loan debt in repayment and an increase in loans in forbearance.

- Borrowers Affected: 35 million

3.5. Changes in Loan Status

Between the second and third financial quarters of 2020, the amount of student loan debt in repayment decreased by 82%, while student debt in forbearance increased by 375%. These changes reflect the immediate impact of the CARES Act on borrowers’ loan statuses.

- Decrease in Repayment: 82%

- Increase in Forbearance: 375%

4. Demographics of Student Loan Borrowers

Understanding the demographics of student loan borrowers is crucial for tailoring effective solutions. This section examines student loan debt across different age groups, genders, races, and levels of education.

4.1. Debt by Age

Student loan debt is prevalent among younger adults, with 25% of those aged 18 to 29 years reporting student loan debt. However, student loan debt also affects older adults, with 6.3% of federal borrowers being 62 years of age and older.

- 18-29 Age Group: 25% with student loan debt

- 62+ Age Group: 6.3% of federal borrowers

4.2. Debt by Gender

Female bachelor’s degree holders are more likely to take out federal student loans than their male counterparts. Approximately 49.3% of female bachelor’s degree holders accept federal student loans, compared to 41.9% of male bachelor’s degree holders.

- Female Bachelor’s: 49.3% accept federal loans

- Male Bachelor’s: 41.9% accept federal loans

4.3. Debt by Race or Ethnicity

Black students are the most likely to borrow federal loans among bachelor’s degree holders, with 82.9% taking out federal loans. Additionally, Black student borrowers owe significantly more than white borrowers four years after graduation.

- Black Bachelor’s: 82.9% accept federal loans

4.4. Debt by Educational Attainment

Borrowers with higher levels of education tend to have higher student loan debt balances. The average federal student loan debt for those with an associate’s degree is $20,340, while bachelor’s degree holders have an average debt of $29,550. Graduate degree holders owe significantly more, with an average debt of up to $102,790.

- Associate’s Degree: $20,340

- Bachelor’s Degree: $29,550

- Graduate Degree: Up to $102,790

5. Types of Student Loans

Understanding the different types of student loans is essential for effective debt management. This section outlines the main categories of student loans, including federal and private loans, as well as specific loan programs.

5.1. Federal Student Loans

Federal student loans are funded by the government and come with certain protections and benefits, such as income-driven repayment plans and loan forgiveness programs. The main types of federal student loans include Stafford Loans, Direct Consolidated Loans, Parent PLUS Loans, and Grad PLUS Loans.

- Stafford Loans: Subsidized and Unsubsidized

- Direct Consolidated Loans: Combine multiple federal loans into one

- Parent PLUS Loans: Borrowed by parents on behalf of their children

- Grad PLUS Loans: For graduate and professional students

5.2. Private Student Loans

Private student loans are offered by banks and other financial institutions. These loans typically have fewer protections and benefits compared to federal loans, but they may be an option for borrowers who have exhausted their federal loan options.

- Offered by: Banks and financial institutions

5.3. Stafford Loans

Stafford Loans are a common type of federal student loan. They can be subsidized, meaning the government pays the interest while the borrower is in school, or unsubsidized, meaning the borrower is responsible for the interest from the time the loan is disbursed.

- Subsidized: Government pays interest while in school

- Unsubsidized: Borrower pays interest from disbursement

5.4. PLUS Loans

PLUS Loans are available to parents of dependent undergraduate students (Parent PLUS Loans) and to graduate or professional students (Grad PLUS Loans). These loans have higher interest rates and fees compared to Stafford Loans.

- Parent PLUS Loans: For parents of undergraduates

- Grad PLUS Loans: For graduate and professional students

5.5. Perkins Loans

Perkins Loans were previously available to students with exceptional financial need, but the program has been discontinued. Some borrowers may still have outstanding Perkins Loans.

- Discontinued Program: Previously for students with financial need

6. Student Loan Forgiveness Programs

Student loan forgiveness programs offer a path to debt relief for borrowers who meet certain eligibility requirements. This section examines the main student loan forgiveness programs and their impact.

6.1. Public Service Loan Forgiveness (PSLF)

The Public Service Loan Forgiveness (PSLF) program forgives the remaining balance on Direct Loans after 120 qualifying monthly payments made under a qualifying repayment plan while working full-time for a qualifying employer.

- Requirements: 120 qualifying payments, full-time work for qualifying employer

6.2. Teacher Loan Forgiveness Program

The Teacher Loan Forgiveness Program offers loan forgiveness to eligible teachers who teach full-time for five complete and consecutive academic years in a low-income school or educational service agency.

- Requirements: Five years of full-time teaching in a low-income school

6.3. Other Forgiveness Programs

In addition to PSLF and the Teacher Loan Forgiveness Program, other forgiveness programs may be available for borrowers in certain professions or with specific circumstances.

- Various Programs: Based on profession or circumstances

6.4. Low Approval Rates

Historically, the approval rates for student loan forgiveness programs, particularly PSLF, have been low. This is often due to complex eligibility requirements and administrative issues.

- Historically Low: Due to complex requirements

6.5. Total Forgiven Loans

Despite the low approval rates, significant amounts of student loans have been forgiven through these programs. As of a certain date, a total of $46.8 billion in federal student loans had been forgiven through PSLF.

- Significant Amounts: Billions of dollars forgiven

7. Navigating Student Loan Debt: Expert Advice from HOW.EDU.VN

At HOW.EDU.VN, our team of over 100 PhDs is dedicated to providing expert guidance on navigating the complexities of student loan debt. We understand the challenges borrowers face and offer personalized advice to help them make informed decisions.

7.1. Comprehensive Debt Analysis

Our experts conduct a thorough analysis of your student loan debt, taking into account factors such as loan types, interest rates, repayment plans, and eligibility for forgiveness programs.

- Thorough Analysis: Loan types, rates, repayment plans, eligibility

7.2. Customized Repayment Strategies

Based on your individual circumstances, we develop customized repayment strategies to help you manage your debt effectively. This may include exploring options such as income-driven repayment plans, loan consolidation, or refinancing.

- Individual Strategies: Income-driven plans, consolidation, refinancing

7.3. Forgiveness Program Guidance

We provide guidance on navigating student loan forgiveness programs, helping you determine your eligibility and complete the necessary paperwork. Our experts can also assist you in understanding the complex requirements and maximizing your chances of approval.

- Expert Guidance: Eligibility, paperwork, maximizing approval chances

7.4. Financial Planning Support

In addition to debt management, we offer financial planning support to help you achieve your long-term financial goals. This may include advice on budgeting, saving, investing, and retirement planning.

- Long-Term Goals: Budgeting, saving, investing, retirement

7.5. Expert Team of PhDs

Our team consists of over 100 PhDs with expertise in various fields, including finance, economics, and education. With their extensive knowledge and experience, they can provide you with the highest quality advice and support.

- Extensive Knowledge: Finance, economics, education

8. Student Loan Debt and the Economy

The impact of student loan debt extends beyond individual borrowers and affects the broader economy. This section explores the economic consequences of student loan debt and its implications for the future.

8.1. Impact on Consumer Spending

High levels of student loan debt can reduce consumer spending, as borrowers have less disposable income to spend on goods and services. This can slow down economic growth and impact various industries.

- Reduced Spending: Impacts economic growth

8.2. Impact on Homeownership

Student loan debt can make it more difficult for borrowers to purchase homes, as lenders may be hesitant to approve mortgages for those with significant student loan obligations. This can impact the housing market and limit opportunities for wealth accumulation.

- Difficult Homeownership: Impacts housing market

8.3. Impact on Retirement Savings

Student loan debt can also affect borrowers’ ability to save for retirement. With a significant portion of their income going towards loan payments, borrowers may have less money available to contribute to retirement accounts, potentially jeopardizing their financial security in the future.

- Reduced Savings: Jeopardizes future security

4. Impact on Entrepreneurship

Student loan debt can deter individuals from starting their own businesses, as they may be risk-averse due to their existing financial obligations. This can stifle innovation and limit job creation.

- Discourages Startups: Limits job creation

8.5. Broader Economic Implications

The cumulative impact of student loan debt on consumer spending, homeownership, retirement savings, and entrepreneurship can have significant consequences for the overall economy. Addressing the student loan debt crisis is essential for fostering sustainable economic growth and prosperity.

- Significant Consequences: Essential for economic growth

9. Student Loan Debt Scams: What to Watch Out For

Unfortunately, the student loan debt crisis has also led to an increase in scams targeting vulnerable borrowers. This section outlines common student loan debt scams and provides advice on how to protect yourself.

9.1. Promises of Debt Forgiveness

Scammers often promise quick and easy debt forgiveness in exchange for upfront fees. However, legitimate debt forgiveness programs typically have strict eligibility requirements and do not require upfront payments.

- Red Flag: Upfront fees for forgiveness

9.2. Bogus Refinancing Offers

Scammers may offer bogus refinancing offers that include excessive upfront fees or unfavorable terms. Borrowers should always research refinancing options carefully and avoid deals that seem too good to be true.

- Red Flag: Excessive fees or unfavorable terms

9.3. Requests for FSA ID Password

The U.S. Department of Education warns that they will never ask you for your FSA ID password. Your FSA ID is like an electronic signature, and you should never share it with anyone.

- Never Share: FSA ID password

9.4. Steps to Take if Scammed

If you suspect you have been scammed, take the following steps immediately:

- Change your FSA ID.

- Contact your student loan servicer and revoke any power of attorney or third-party authorization agreements.

- Contact your bank or financial service to cancel any payments to any student debt relief companies.

- File a report of identity theft with the Federal Trade Commission.

- Submit a complaint with the Federal Student Aid Feedback System regarding suspicious activity.

- Immediate Actions: Change FSA ID, contact servicer and bank, file reports

9.5. Reporting Suspicious Activity

It’s crucial to report any suspicious activity to the appropriate authorities, such as the Federal Trade Commission and the Federal Student Aid Feedback System. This can help protect yourself and others from becoming victims of student loan debt scams.

- Report to: FTC and Federal Student Aid Feedback System

10. Seeking Professional Assistance

Navigating the complexities of student loan debt can be overwhelming, and seeking professional assistance is often the best course of action. HOW.EDU.VN offers expert guidance and support to help you manage your student loan debt effectively.

10.1. Benefits of Professional Guidance

Professional guidance can provide numerous benefits, including:

- Expert Advice: Informed decision-making

- Customized Strategies: Tailored to individual circumstances

- Time Savings: Efficient debt management

- Stress Reduction: Alleviating financial anxiety

10.2. HOW.EDU.VN’s Expert Team

Our team of over 100 PhDs has extensive knowledge and experience in student loan debt management. We stay up-to-date on the latest regulations and programs, ensuring that you receive the most accurate and effective advice.

- Up-to-Date: Latest regulations and programs

10.3. Personalized Solutions

We understand that every borrower’s situation is unique, and we tailor our solutions to meet your specific needs and goals. Whether you need help with repayment strategies, forgiveness program guidance, or financial planning support, we are here to assist you.

- Tailored Solutions: Meeting specific needs and goals

10.4. Contact Information

To learn more about how HOW.EDU.VN can help you navigate your student loan debt, please contact us at:

- Address: 456 Expertise Plaza, Consult City, CA 90210, United States

- WhatsApp: +1 (310) 555-1212

- Website: HOW.EDU.VN

10.5. Take Control of Your Future

Don’t let student loan debt hold you back from achieving your financial goals. Contact HOW.EDU.VN today and take control of your future.

FAQ: Student Loan Debt

Q1: How much student loan debt is there in the United States?

A1: As of 2024, the total student loan debt in the United States is approximately $1.777 trillion.

Q2: What is the average federal student loan debt balance?

A2: The average federal student loan debt balance is $38,375.

Q3: What percentage of federal student loans are in default?

A3: As of 2024’s fourth financial quarter, 4.86% of federal student loan dollars were in default.

Q4: How can HOW.EDU.VN help with student loan debt?

A4: HOW.EDU.VN provides expert guidance on navigating student loan debt through comprehensive debt analysis, customized repayment strategies, and forgiveness program guidance.

Q5: What is the Public Service Loan Forgiveness (PSLF) program?

A5: PSLF forgives the remaining balance on Direct Loans after 120 qualifying monthly payments made under a qualifying repayment plan while working full-time for a qualifying employer.

Q6: Are there scams related to student loan debt?

A6: Yes, there are scams promising quick debt forgiveness or bogus refinancing offers. Always be cautious and avoid upfront fees.

Q7: What should I do if I suspect I’ve been scammed?

A7: Change your FSA ID, contact your student loan servicer and bank, file a report with the Federal Trade Commission, and submit a complaint with the Federal Student Aid Feedback System.

Q8: How does student loan debt impact the economy?

A8: Student loan debt can reduce consumer spending, impact homeownership, affect retirement savings, and deter entrepreneurship.

Q9: What types of student loans are available?

A9: There are federal student loans (Stafford Loans, Direct Consolidated Loans, Parent PLUS Loans, and Grad PLUS Loans) and private student loans.

Q10: Why should I seek professional assistance for managing student loan debt?

A10: Professional guidance provides expert advice, customized strategies, time savings, and stress reduction, ensuring effective debt management tailored to your unique circumstances.

Don’t let student loan debt overwhelm you. Contact the experts at HOW.EDU.VN for personalized guidance and support.

Address: 456 Expertise Plaza, Consult City, CA 90210, United States

WhatsApp: +1 (310) 555-1212

Website: how.edu.vn