How much is car insurance for an 18-year-old? At HOW.EDU.VN, we understand that insuring a young driver can be a significant financial concern for families, and we’re here to provide clarity and solutions. This article dives deep into the costs associated with car insurance for 18-year-olds, offering expert advice on how to navigate the insurance landscape and secure the most affordable coverage. By understanding the factors that influence insurance premiums and exploring available discounts, families can make informed decisions that protect both their young drivers and their wallets. Let’s explore teen driver insurance rates and the implications of young driver coverage so you’re equipped to find comprehensive auto coverage.

1. Understanding the High Cost of Car Insurance for 18-Year-Olds

Eighteen-year-olds face some of the highest car insurance rates due to their inexperience and statistically higher risk of accidents. Insurance companies view young drivers as a greater liability because they lack driving experience, tend to engage in riskier behaviors, and are more prone to distractions. According to the Insurance Institute for Highway Safety (IIHS), the fatal crash rate per mile driven is significantly higher for teenagers than for drivers aged 20 and older. This increased risk translates directly into higher premiums.

1.1. Statistical Risks Associated with Young Drivers

Several factors contribute to the elevated risk profile of young drivers:

- Inexperience: Lack of experience in handling various driving conditions.

- Risk-Taking Behavior: Higher likelihood of speeding, reckless driving, and impaired driving.

- Distractions: Increased susceptibility to distractions like cell phones and passengers.

- Poor Judgment: Less developed decision-making skills in critical driving situations.

1.2. Impact on Insurance Premiums

Given these risks, insurance companies charge higher premiums to mitigate potential payouts from accidents involving 18-year-old drivers. This can be financially challenging for both the young drivers and their families.

2. Average Car Insurance Costs for 18-Year-Olds

The cost of car insurance for an 18-year-old can vary significantly depending on whether they are added to a parent’s policy or purchase their own. Generally, it is more economical to add a young driver to an existing policy.

2.1. Adding to a Parent’s Policy

Adding an 18-year-old to a parent’s car insurance policy typically results in a lower premium than if the teen were to purchase their own policy. Forbes Advisor’s analysis indicates that the average annual cost to add an 18-year-old to a parent’s policy is around $2,103, or about $175 per month.

2.2. Standalone Policy for 18-Year-Olds

An 18-year-old buying their own car insurance policy can expect to pay significantly more. The average annual cost for a standalone policy is approximately $6,147, which translates to about $512 per month. This substantial difference highlights the financial advantage of remaining on a parent’s policy, if possible.

2.3. Total Family Cost

When adding an 18-year-old driver to a family policy, the overall cost of the policy will increase. On average, a parent’s auto insurance policy with an 18-year-old driver included costs around $5,065 per year. This figure underscores the need to budget for the additional expense of insuring a young driver.

3. Factors Influencing Car Insurance Costs for 18-Year-Olds

Several factors influence the cost of car insurance for 18-year-olds. Understanding these factors can help families take proactive steps to lower their premiums.

3.1. Age and Experience

Age is a primary factor in determining insurance rates. Younger drivers, especially those with limited experience, are considered higher risks. As drivers gain experience and maintain a clean driving record, their rates tend to decrease over time.

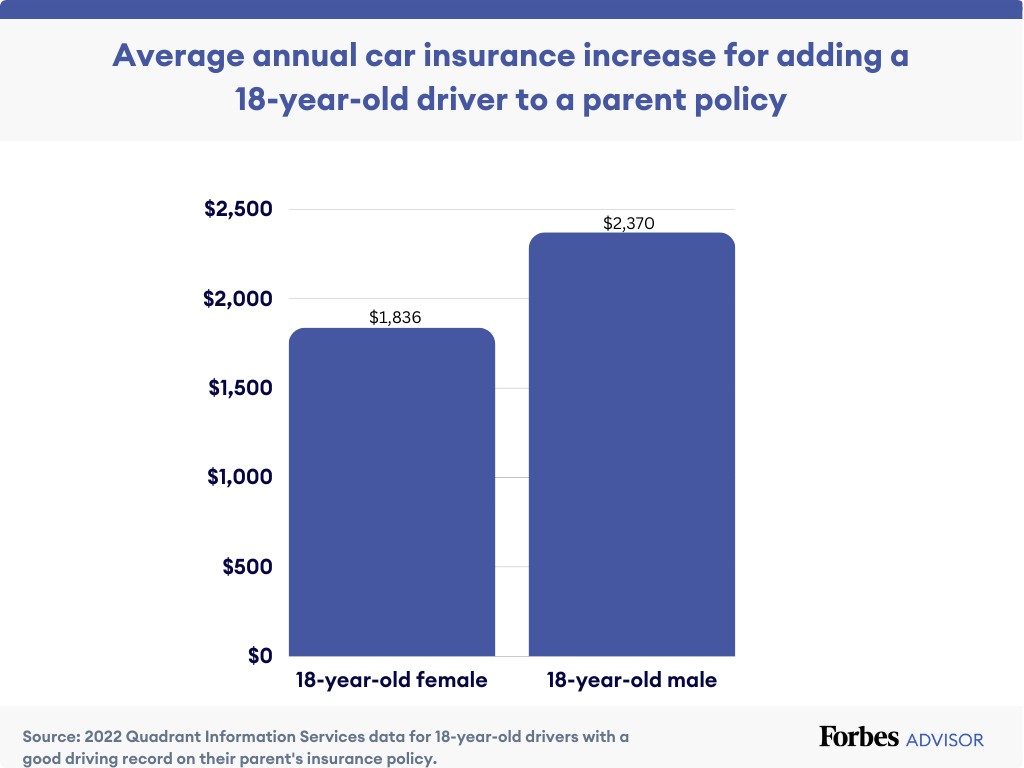

3.2. Gender

Gender also plays a role in insurance pricing. Statistically, young male drivers are more likely to engage in risky driving behaviors and be involved in accidents, leading to higher premiums compared to their female counterparts.

3.3. Location

The geographic location of the driver can significantly impact insurance costs. Urban areas with higher traffic density, accident rates, and vehicle theft rates typically have higher premiums. Additionally, state laws and regulations can influence insurance prices.

3.4. Vehicle Type

The type of vehicle insured affects the cost of coverage. Sports cars and high-performance vehicles generally have higher premiums due to their increased risk of accidents and theft. Conversely, safer, more practical vehicles tend to have lower insurance costs.

3.5. Driving Record

A clean driving record is essential for obtaining affordable insurance rates. Accidents, traffic violations, and DUI convictions can lead to substantial premium increases. Maintaining a safe driving record is crucial for keeping insurance costs down.

3.6. Coverage Options

The level of coverage selected also influences the overall cost of insurance. Higher coverage limits and additional features like collision and comprehensive coverage will result in higher premiums. Balancing adequate protection with affordability is a key consideration.

4. Finding the Cheapest Car Insurance for 18-Year-Olds

Despite the high costs associated with insuring young drivers, there are strategies to find more affordable coverage. Shopping around, exploring discounts, and making informed decisions about coverage can help lower premiums.

4.1. Comparison Shopping

One of the most effective ways to find cheap car insurance is to compare quotes from multiple companies. Rates can vary significantly between insurers, so it’s important to get quotes from several providers to find the best deal. Online comparison tools and independent insurance agents can assist in this process.

4.2. Available Discounts

Numerous discounts are available that can help lower the cost of car insurance for 18-year-olds. Taking advantage of these discounts can lead to significant savings.

4.2.1. Good Student Discount

Many insurance companies offer a good student discount for young drivers who maintain a certain GPA or excel academically. Typically, students need to provide proof of good grades, such as a transcript or report card, to qualify for this discount. Forbes Advisor’s analysis indicates that good student discounts average around 4% savings.

4.2.2. Student Away From Home Discount

If an 18-year-old is attending college away from home and does not regularly drive the insured vehicle, they may be eligible for a student away from home discount. This discount recognizes the reduced risk associated with the student spending less time on the road. According to Forbes Advisor’s analysis, student away from home discounts average about 8% savings.

4.2.3. Driver Training Discount

Completing an approved driver training program can also qualify an 18-year-old for a discount. These programs help young drivers develop safe driving habits and skills, making them less likely to be involved in accidents.

4.3. Choosing the Right Coverage

Selecting the appropriate level of coverage is essential for balancing protection and affordability. While it may be tempting to opt for the minimum coverage required by law to save money, this can leave drivers vulnerable to significant financial losses in the event of an accident.

4.3.1. Liability Coverage

Liability coverage protects drivers from financial responsibility if they cause an accident that results in injuries or property damage to others. It is typically required by law and is essential for protecting assets.

4.3.2. Collision Coverage

Collision coverage pays for damages to the insured vehicle resulting from a collision with another vehicle or object. This coverage is optional but can be valuable for repairing or replacing a vehicle after an accident.

4.3.3. Comprehensive Coverage

Comprehensive coverage protects against damages to the insured vehicle caused by non-collision events, such as theft, vandalism, fire, or natural disasters. This coverage is also optional but can provide peace of mind.

4.4. Increasing Deductibles

Choosing a higher deductible can lower insurance premiums. A deductible is the amount a policyholder pays out-of-pocket before the insurance company covers the remaining costs. By increasing the deductible, policyholders can reduce their premiums, but they will need to be prepared to pay more out-of-pocket in the event of a claim.

4.5. Safe Driving Practices

Encouraging safe driving practices among 18-year-olds can lead to lower insurance rates over time. Safe driving habits include:

- Avoiding distractions while driving.

- Obeying traffic laws and speed limits.

- Maintaining a safe following distance.

- Driving defensively and being aware of surroundings.

- Avoiding driving under the influence of alcohol or drugs.

5. Car Insurance Companies with Competitive Rates for 18-Year-Olds

Several insurance companies offer competitive rates for 18-year-olds. These companies may have specific programs or discounts tailored to young drivers.

5.1. USAA

USAA is consistently ranked as one of the cheapest car insurance companies for both adding an 18-year-old to a parent’s policy and for standalone policies. However, USAA coverage is limited to members of the military, veterans, and their immediate families.

5.2. Erie Insurance

Erie Insurance is another top choice for affordable car insurance for 18-year-olds. Erie offers competitive rates and a variety of discounts, making it a popular option for families.

5.3. Geico

Geico is a well-known insurance provider that offers competitive rates for young drivers. Geico also provides numerous discounts, including good student discounts and driver training discounts.

5.4. State Farm

State Farm is a reputable insurance company with a wide range of coverage options and discounts. State Farm’s Steer Clear program offers additional discounts for young drivers who maintain a clean driving record.

6. Impact of State Laws on Car Insurance Costs

State laws and regulations can significantly impact car insurance costs. Some states have higher minimum coverage requirements, which can lead to higher premiums. Additionally, states with no-fault insurance laws may have different cost structures than states with tort-based systems.

6.1. Minimum Coverage Requirements

Most states have minimum liability coverage requirements that drivers must meet. These requirements specify the minimum amount of coverage for bodily injury and property damage liability. States with higher minimums may have higher average insurance costs.

6.2. No-Fault vs. Tort-Based Systems

In no-fault states, drivers typically file claims with their own insurance company regardless of who was at fault in the accident. In tort-based systems, drivers can sue the at-fault party for damages. No-fault systems may have different cost structures and coverage requirements than tort-based systems.

6.3. State-Specific Discounts

Some states may offer specific discounts or programs to help lower the cost of car insurance for young drivers. These may include state-sponsored driver education programs or discounts for installing certain safety features in vehicles.

7. Long-Term Strategies for Reducing Car Insurance Costs

In addition to short-term strategies like comparison shopping and exploring discounts, there are long-term steps families can take to reduce car insurance costs for 18-year-olds.

7.1. Maintaining a Clean Driving Record

The most effective way to lower insurance rates over time is to maintain a clean driving record. Avoiding accidents, traffic violations, and DUI convictions can lead to significant savings.

7.2. Gradual Increase in Coverage

As young drivers gain experience and demonstrate responsible driving habits, families can gradually increase their coverage limits and add additional features like collision and comprehensive coverage.

7.3. Investing in Vehicle Safety

Investing in vehicles with advanced safety features can also help lower insurance costs. Features like anti-lock brakes, electronic stability control, and advanced driver assistance systems can reduce the risk of accidents and injuries.

7.4. Continuous Education and Training

Encouraging young drivers to participate in continuous education and training programs can improve their driving skills and reduce their risk of accidents. These programs may also qualify drivers for additional discounts.

8. How HOW.EDU.VN Can Help You Find the Best Car Insurance

Navigating the complexities of car insurance can be challenging, especially when insuring a young driver. At HOW.EDU.VN, we connect you with top experts, including experienced insurance advisors, who can provide personalized guidance and support.

8.1. Access to Expert Advisors

Our platform offers access to a network of over 100 PhDs and experts across various fields, including insurance. These experts can provide in-depth knowledge and insights to help you make informed decisions about car insurance.

8.2. Personalized Consultations

We offer personalized consultation services to address your specific needs and concerns. Our experts can assess your situation, evaluate your coverage options, and recommend the most suitable insurance solutions.

8.3. Comprehensive Resources

HOW.EDU.VN provides a wealth of resources, including articles, guides, and tools, to help you understand car insurance and make informed decisions.

8.4. Continuous Support

Our team is dedicated to providing continuous support throughout your insurance journey. Whether you have questions about coverage, discounts, or claims, we are here to help.

9. Real-Life Examples and Case Studies

To illustrate the value of expert guidance, consider the following real-life examples:

9.1. Case Study 1: The Smith Family

The Smith family was struggling to find affordable car insurance for their 18-year-old son, who had recently obtained his driver’s license. After consulting with an insurance expert through HOW.EDU.VN, they were able to identify several discounts and coverage options that significantly lowered their premiums.

9.2. Case Study 2: The Johnson Family

The Johnson family’s 18-year-old daughter was heading off to college and needed car insurance coverage. By consulting with an expert advisor, they were able to secure a student away from home discount and adjust their coverage to meet their specific needs.

10. Call to Action: Get Expert Car Insurance Advice Today

Don’t let the high cost of car insurance for 18-year-olds overwhelm you. At HOW.EDU.VN, we are here to help you navigate the insurance landscape and find the most affordable coverage for your family.

- Connect with our Experts: Gain access to personalized advice from over 100 PhDs and experts.

- Get Personalized Consultations: Receive tailored recommendations to meet your specific needs.

- Explore Comprehensive Resources: Access articles, guides, and tools to make informed decisions.

Contact us today at 456 Expertise Plaza, Consult City, CA 90210, United States. Reach out via Whatsapp at +1 (310) 555-1212, or visit our website at how.edu.vn for expert car insurance advice. Because securing cheap auto insurance is not impossible.

11. FAQs About Car Insurance for 18-Year-Olds

11.1. Why is car insurance so expensive for 18-year-olds?

Car insurance is expensive for 18-year-olds because teenage drivers are more prone to be in accidents. The Insurance Institute for Highway Safety finds that the number of auto accidents and fatal collisions is disproportionately high for teenage drivers. The fatal crash rate per miles driven is nearly three times for drivers ages 16 to 19 compared to drivers ages 20 and older.

11.2. Can you add an 18-year-old to an existing policy?

Yes, you can add an 18-year-old to an existing car insurance policy, and it’s probably a more affordable way to insure your teen. Adding an 18-year-old driver to a parent policy usually is much cheaper than the teen buying their own policy.

11.3. At what age will car insurance rates start to go down?

Car insurance rates gradually decline each year as teens get older, and by age 21, the cost of adding a teen to a parent policy is nearly half the cost of an 18-year-old. Parents pay an average of $2,103 per year for adding an 18-year-old and only $1,110 for adding a 21-year-old.

11.4. Will safe driving influence the cost of car insurance for an 18-year-old driver?

Yes, safe driving can influence the cost of car insurance for an 18-year-old, and in a good way. Being a safe driver signals that you’re a low risk, which usually results in lower car insurance rates. And some companies offer safe driving discounts for young drivers.

11.5. What is a good student discount for car insurance?

A good student discount is a discount offered by car insurance companies to young drivers who maintain good grades. This recognizes that students who perform well academically may also be more responsible drivers.

11.6. How does gender affect car insurance rates for 18-year-olds?

Young male drivers tend to pay higher car insurance rates than young female drivers because they are statistically more likely to be involved in accidents and engage in risky driving behaviors.

11.7. What types of cars are cheaper to insure for young drivers?

Safer, more practical vehicles tend to have lower insurance costs. Avoid sports cars and high-performance vehicles, which generally have higher premiums due to their increased risk of accidents and theft.

11.8. What is comprehensive coverage?

Comprehensive coverage protects against damages to the insured vehicle caused by non-collision events, such as theft, vandalism, fire, or natural disasters. This coverage is optional but can provide peace of mind.

11.9. How can I lower my car insurance deductible?

Choosing a higher deductible can lower insurance premiums. A deductible is the amount a policyholder pays out-of-pocket before the insurance company covers the remaining costs.

11.10. Is it better for an 18-year-old to be on their parent’s policy or get their own?

It is generally more affordable for an 18-year-old to be added to their parent’s car insurance policy rather than purchasing their own standalone policy. The average annual cost for a standalone policy is approximately $6,147, while adding to a parent’s policy costs around $2,103.

By understanding these factors and taking proactive steps, families can navigate the complexities of car insurance for 18-year-olds and secure affordable coverage.